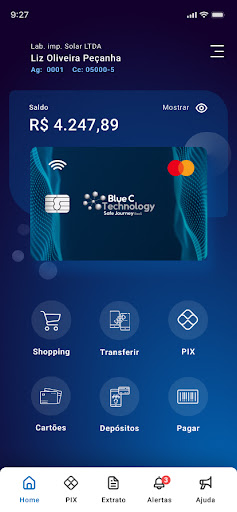

The payment account is an account that can be used by the customer to make withdrawals, bill payments and payments of transactions carried out by debit or credit cards, or to carry out transfers between accounts maintained at the same institution and at other institutions. payment services or financial institutions (TED and DOC).Target AudienceThere is no specific age group or type of audience defined. The payment account is aimed at all those who wish to take advantage of its possibilities.DigitalThe payment account is intended to make life easier for its holders. Everything related to it – opening, operations, relationship between client and institution – can be done digitally.Where are they available?Payment accounts can be offered by payment institutions (PIs), banks, credit unions and other financial institutions.Prepaid or postpaidThey can be classified as pre-paid accounts – intended for making payments using an amount previously contributed by the customer – or post-paid payment accounts – which do not depend on a previous contribution of funds, as is the case with credit cards.the ratesServices linked to postpaid payment accounts are considered priority services and the fees subject to collection are standardized in Table I of Resolution No. 3,919/10, with definition of the triggering events.Those linked to prepaid payment accounts are considered differentiated by the same standard. The collection of fees on them is more flexible, there is no standardization by the National Monetary Council (CMN) or the Central Bank, including in relation to withdrawals, statements and transfers.The required documentsPrepaid payment accounts that have a balance limited to BRL 5,000 can be opened in a simple way. For individuals, full name and CPF are required. The institution where the account will be opened may require additional documents, if deemed necessary.For payment accounts that have a balance with a limit greater than R$ 5 thousand, other documents are required. The complete list can be found in Circular nº 3.680/2013.ProtectionFunds held in payment accounts do not respond directly to any obligation of the payment institution and cannot be subject to arrest, kidnapping, search and seizure or any other act caused by debts for which IP is responsible; and do not form part of the institutions assets for the purpose of bankruptcy or judicial and extrajudicial liquidation.In addition, the funds are allocated in a specific account held at the Central Bank or invested in Federal Government Securities, which provides security for depositors.And it is always good to emphasize that the citizen has free will to, in any situation, decide without any kind of coercion on the opening, maintenance, closing or transfer of any account of which he is the holder.